What is Supply

In Economics, supply refers to the willingness and ability of producers to produce a given product at any given price level over a time period, ceteris paribus.

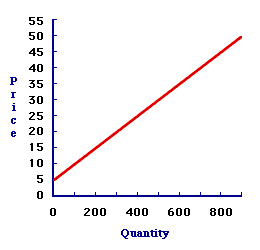

Supply is directly proportional to price in a market. For instance, when the price of an item increases, producers are more willing and able to produce that item.

A illustration of the supply curve is as follows.

Fig1:

Determinants of Supply

Supply in a market is influenced by a variety of non-price factors.

Change in Technology: this influences the quality and quantity of factors of production (land, labor, capital, enterprise) in an economy. With better technology there is better capital in the economy which allows for greater supply of products.

Number of producers: the larger the number of firms in the market, the greater the amount of supply for a given product.

Cost of production: Cost of production is inversely related to supply. If the cost of producing an item is low, producers can supply more of that item at a given price, ceteris paribus.

Tax/subsidy: Taxes and subsidies are price controls introduced by government which can influence the cost of production. A tax raises the cost of production and thus decreases supply. The subsidy reduces cost of production and increases supply.

by Quintessential Education

join our economics tuition and resources!